Money may not buy love, but it appears to buy years.

Money may not buy love, but it appears to buy years.

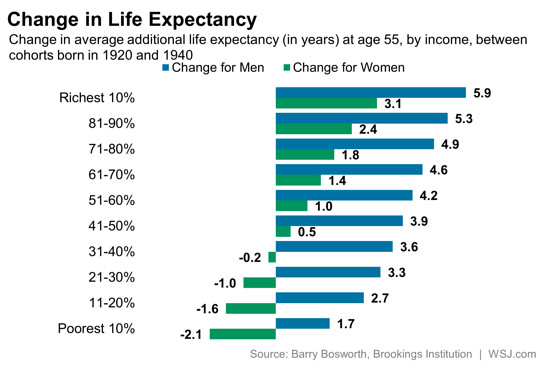

Economist Barry Bosworth at the Brookings Institution crunched the numbers and found that the richer you are, the longer you’ll live. And it’s a gap that is widening, particularly among women.

Mr. Bosworth parsed this data from the University of Michigan’s Health and Retirement Study, a survey that tracks the health and work-life of 26,000 Americans as they age and retire. It is especially valuable as it tracks the same individuals every two years in what’s known as a longitudinal study, to see how their lives unfold.

The good news is that men of all incomes are living longer. Yet the data shows that the life expectancy of the wealthy is growing much faster than the life expectancy of the poor.

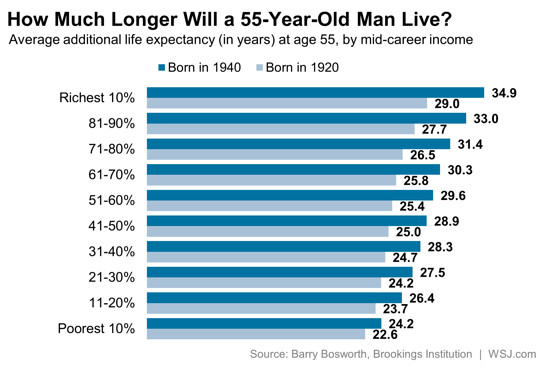

Here’s the sort of detail this remarkable data set can show. You can look at a man born in 1940 and see that during the 1980s, the mid-point of his career, his income was in the top 10% for his age group. If that man lives to age 55 he can expect to live an additional 34.9 years, or to the age of 89.9. That’s six years longer than a man whose career followed the same arc, but who was born in 1920.

For men who were in the poorest 10%, they can expect to live another 24 years, only a year and a half longer than his 1920s counterpart.

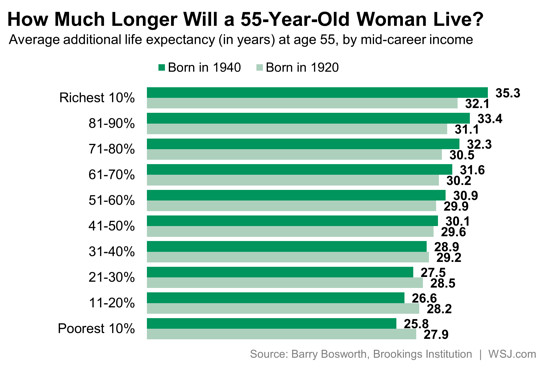

The story is rather different for women. At every income level, for both those born in 1920 and 1940, women live longer than men. But for women, the longevity and income trends are even more striking. While the wealthiest women from the 1940s are living longer, the poorest 40% are seeing life expectancy decline from the previous generation.

“At the bottom of the distribution, life is not improving rapidly for women anymore,” said Mr. Bosworth. “Smoking stands out as a possibility. It’s much more common among women at lower income levels.”

Mr. Bosworth’s findings build off earlier research from Hilary Waldron at the Social Security Administration who has also documented the widening gap at the interplay of incomes and longevity. Researchers studying life expectancy use actuarial calculations for their estimates, as precise outcomes cannot be known until an entire generation has passed away. He analyzed the data, along with Kathleen Burke at the Consumer Financial Protection Bureau, to evaluate a common proposal to keep Social Security in balance as the population ages: to simply raise the retirement age.

“If it turns out people at the bottom are not having an increase in life expectancy. They are getting a real reduction” in Social Security benefits as a result, said Mr. Bosworth. “They’re going to get it for less years.”

Take the example above. A wealthy man, born in 1920 who retired at age 65, could expect to draw Social Security for 19 years. His son, born in 1940 and retired at age 67, could expect to draw benefits for 24 years. Yes, he retired later, but he’s living longer.

This would not be true for men and women at the bottom. They would draw Social Security for less years, if the retirement age rises, and their longevity does not.

“It’s really hard to come up with some effective means of trying to equalize this,” said Mr. Bosworth, “and that’s a serious concern.”