Thinking about where to put your real estate dollars for the best returns in 2026? You've come to the right place. I’ve spent a lot of time digging into the numbers and looking at what makes a city a winner for investors. Based on my research and what the experts are saying, the 20 best US cities to invest in real estate in 2026 are those showing strong job growth, attracting new people, and offering good value for your money. These are places where your investment is likely to grow and bring in steady income.

The 20 Best US Cities to Invest in Real Estate in 2026

The real estate market can feel like a guessing game, right? But for me, it's about understanding the underlying forces. When a city has a healthy economy with lots of jobs, people want to live there. More people means more renters, which means more income for you. And when cities are bringing in new residents, especially those with good jobs, property values tend to go up over time. That's what we call capital appreciation.

So, what makes these specific cities stand out for 2026? It's a combination of factors. We're seeing big companies moving in, creating thousands of jobs. We're also seeing people move from more expensive areas to find a better quality of life and more affordable housing. And importantly, these cities often have a good rent-to-price ratio, meaning the rent you can charge is a healthy percentage of the property's cost. This is crucial for generating immediate cash flow.

Let's dive into the cities that are poised to be real estate powerhouses. I’ve broken them down to give you a clearer picture of where the opportunities lie.

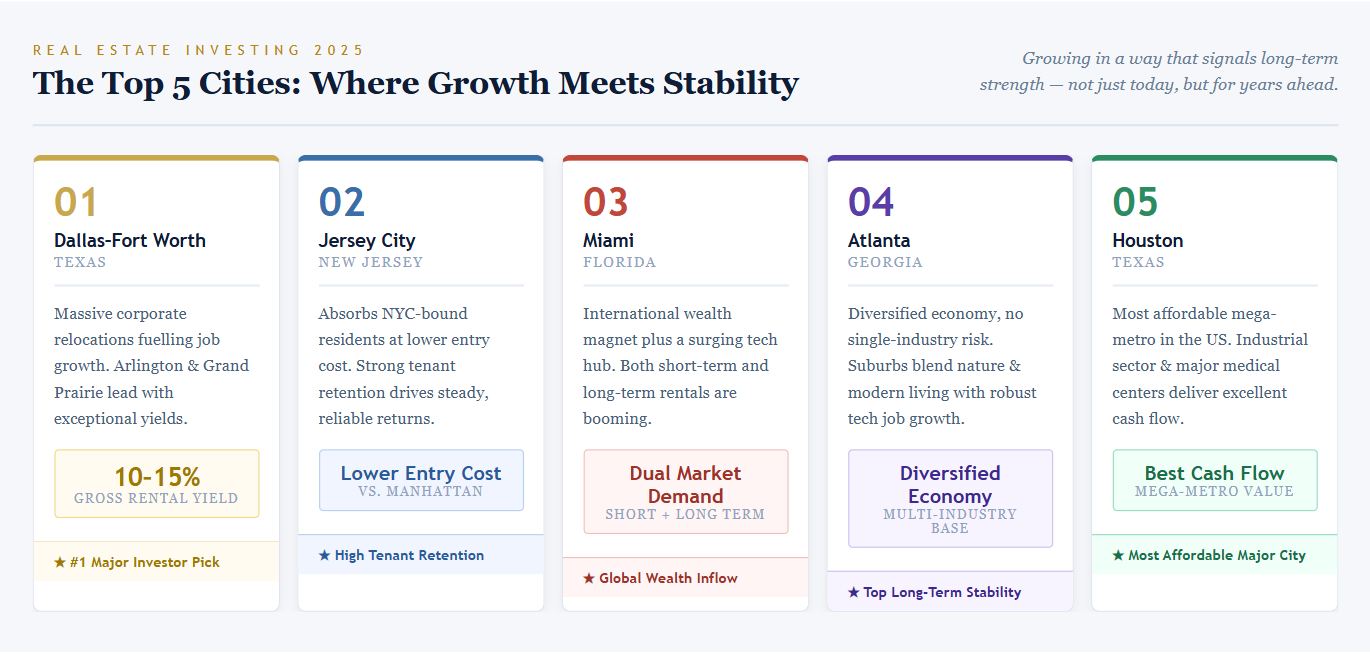

Top Cities to Invest in Real Estate: Where Growth Meets Stability

These cities are like the MVPs of real estate investing right now. They’re not just growing; they’re growing in a way that suggests they’ll be strong for a long time.

- Dallas-Fort Worth, Texas: This metroplex is absolutely on fire. It's consistently ranked as the top market for big-time investors, and for good reason. Massive corporate relocations are bringing in tons of jobs, and in areas like Arlington and Grand Prairie, you can see gross rental yields (that’s the rent you earn before expenses) hitting an impressive 10% to 15%. This means your money is working hard for you from day one.

- Jersey City, New Jersey: Don't let its proximity to NYC fool you. Jersey City is a strong investment on its own. It’s soaking up people who want to live near the Big Apple but can't afford the Manhattan price tag. The lower entry costs and strong tenant retention make it a smart move for steady returns.

- Miami, Florida: Miami continues to be a magnet for international wealth. Combine that with a rapidly growing local tech hub, and you've got a recipe for high demand. Both short-term vacation rentals and long-term residential leases are seeing exceptional activity.

- Atlanta, Georgia: Atlanta’s strength lies in its diversified economy. It’s not reliant on just one industry. Plus, its suburbs are expanding rapidly, and many neighborhoods are blending nature with modern living, all while fostering robust tech job growth. This makes it a top-tier choice for long-term stability.

- Houston, Texas: If affordability in a major city is what you're after, Houston is it. It’s one of the most affordable mega-metros out there. With strong job bases in industrial sectors and major medical centers, Houston offers excellent opportunities for cash flow.

High-Growth Sun Belt Cities: Riding the Wave of Popularity

The Sun Belt, the southern and southwestern parts of the US, has been a hotbed for growth, and 2026 is no exception. These cities are attracting new residents with their climates, lower costs of living, and expanding job markets.

- Phoenix, Arizona: Phoenix is a prime example of how manufacturing can drive growth. The expanding semiconductor manufacturing ecosystem is creating jobs, and the population keeps growing, leading to sustained demand for housing.

- Nashville, Tennessee: Music City is more than just music. Major companies are setting up shop here, and the hospitality sector is booming, which fuels demand for short-term rentals.

- Orlando, Florida: Known for theme parks, Orlando is also a fantastic place for investors. It's ranked #1 for raw land investment and offers strong potential for long-term residential vacation rentals.

- San Antonio, Texas: According to Zillow, San Antonio is a buyer-friendly city. This means prices haven't skyrocketed as much as in other places, and there's less competition for buyers, making it a more accessible market.

- Austin, Texas: Despite some price adjustments, Austin’s tech-sector employment density keeps demand high, especially for new home construction. It's a market that rewards those who understand its dynamic.

- Tampa, Florida: Tampa is a great place to hedge against inflation. High rental demand and investor-friendly tax structures make it an attractive option for preserving and growing your wealth.

- Jacksonville, Florida: If South Florida feels too expensive, Jacksonville offers a more affordable entry point with significant growth in its coastal logistics sector.

- Raleigh, North Carolina: Home to Research Triangle Park, Raleigh benefits from a highly educated workforce and high-income tenant bases. This translates to stable rental income.

High-Yield Secondary & Pivot Cities: Smart Money Finds Value

Sometimes, the best deals aren't in the biggest headlines. These cities might be considered “secondary” markets, but they offer excellent value and strong returns for savvy investors.

- Indianapolis, Indiana: Zillow named Indianapolis the #1 most buyer-friendly metro, and I agree. It offers high rental yields and affordable entry costs, making it a fantastic spot for immediate cash flow.

- Northwest Arkansas (Fayetteville/Bentonville): With giants like Walmart headquartered here, rental yields in this region can reach 9% to 12%. The corporate presence creates a steady stream of renters.

- Colorado Springs, Colorado: The strong military presence and the appeal of an outdoor lifestyle make this city a consistent performer. East Colorado Springs, in particular, is a top pick.

- Birmingham, Alabama: Realtor.com highlighted Birmingham for its affordable multi-family opportunities. This means you can often buy buildings with multiple units, maximizing your potential for strong monthly cash flow.

- Salt Lake City, Utah: This city is a fascinating blend of a tech-focused economy and explosive organic population growth. The combination is driving demand and appreciation.

- Lubbock, Texas: With Texas Tech University and growing medical centers, Lubbock is a prime market for student housing and rentals for healthcare professionals, often yielding stable double-digit returns.

- Savannah, Georgia: The expansion of its logistics port combined with a thriving tourism industry creates a dynamic rental market that caters to both long-term residents and short-term visitors.

Maximizing Immediate Cash Flow: Your Top Cash-Flow Powerhouses for 2026

For many investors, the goal is to see money in their bank account every month. If that’s your priority, focusing on markets with a high rent-to-price ratio, low property taxes, and strong tenant demand is key. Based on current 2026 metrics, here are the top 5 cities that really shine for immediate monthly cash flow from single-family rentals (SFRs).

| City | Why It Wins for Cash Flow | Average SFR Price (approx.) | Target Gross Yield | Best Submarkets |

|---|---|---|---|---|

| Indianapolis, IN | Lowest entry barrier, high rent-to-price ratios. | $220,000 – $260,000 | 9% – 11% | Lawrence, Warren Township, Southport |

| Houston, TX | No state income tax, massive blue-collar tenant pool. | $260,000 – $310,000 | 8.5% – 10.5% | Katy (older inventory), Spring, Pasadena |

| Birmingham, AL | Exceptionally low property taxes maximize net cash flow. | $160,000 – $210,000 | 10% – 12% | Center Point, Roebuck, Hüeysville |

| San Antonio, TX | Heavy military and healthcare presence ensures low vacancy. | $240,000 – $280,000 | 8% – 9.5% | Converse, Live Oak, West San Antonio |

| Lubbock, TX | Texas Tech and medical centers drive reliable, high-yield rentals. | $180,000 – $230,000 | 9.5% – 11.5% | Tech Terrace, Medical District |

My take on this? Indianapolis and Birmingham really stand out for their ability to put cash in your pocket quickly because the cost of entry is lower, and expenses like property taxes are also manageable. Houston and San Antonio offer that solid Texas advantage with no income tax and strong job markets that keep renters in place. Lubbock is a fantastic niche play if you're looking at the student or healthcare worker market.

When I look at these markets, I see not just numbers, but communities. I see people needing places to live, growing families, and businesses expanding. That’s the human element that drives real estate.

Choosing the right city is just the first step. Your success will also depend on your specific investment strategy, how you manage your properties, and how you navigate local market conditions. But by focusing on these 20 best US cities to invest in real estate in 2026, you're setting yourself up for a strong and profitable future.

VS

Out‑of‑State investors can compare Converse’s affordable rental with stronger cap rate vs San Antonio’s larger B+ property with steady returns. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Want Stronger Returns? Invest Where the Housing Market’s Growing

Turnkey rental properties in fast-growing housing markets offer a powerful way to generate passive income with minimal hassle.

Work with Norada Real Estate to find stable, cash-flowing markets beyond the bubble zones—so you can build wealth without the risks of ultra-competitive areas.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Speak to a Norada Investment Counselor today (No Obligation):

(800) 611-3060

Recommended Read:

- Best Cities for Turnkey Real Estate Investment in 2026

- Top Markets for Out-of-State Real Estate Investing in 2026

- Best Cities to Buy Investment Properties in 2026

- Best Cities to Buy Multi-Family Homes for Investment in 2026

- Best Cities to Buy Real Estate for Investment in 2026

- 10 Cities With the Highest Demand for Rental Properties in 2026

- 20 Cheapest States to Buy a House in 2026

- Best States to Buy a House in 2026

- Best Cities to Buy a House for Investment in 2026

- Best Cities to Buy a House For Rental Income in 2026

- Best Cities to Invest in Real Estate in 2026

- Should You Invest in the Austin or Raleigh Real Estate Market in 2026?

- Dallas vs. Houston: Which City Offers Better Returns for Real Estate Investors

- Single-Family vs. Townhome: Which is the Real Cash Flow Winner for Investors?

- 5 Hottest Florida and Texas Markets for Real Estate Investors in 2025

- Best Places to Invest in Real Estate: November 2024 Hotspots

- How to Secure Your Retirement With Cash-Flowing Rental Properties

- Best Places to Invest in Single-Family Rental Properties in 2025

- 5 Hottest Real Estate Markets for Buyers & Investors in 2025