For most of my post college life, I’ve had a drastically larger exposure to real estate over stocks. I needed a place to live so I figured it was better to pay down a mortgage than to pay someone rent. When it was time to buy another property, I simply rented out my old place for positive cash flow, and enjoyed my new place until it was time to rent it out again and buy a new place.

I’ve gone through this buy-rent-buy cycle three times now, and it’s been by far the easiest way to make and save several million in tax-advantageous dollars. Within the next five years, our plan is to go through another cycle and buy a Hawaiian beach property and rent out our current San Francisco primary residence.

Now that my exposure to stocks and real estate are more equal after the sale of a SF rental in 2017, I’ve had time to think about the two asset classes more objectively. And during this time, I’ve noticed anti-housing crusaders reach deafening levels!

The main reason why there is so much rage against real estate in expensive cities is due to the human condition.

Why Real Estate Will Always Be More Desirable Than Stocks

You crave what you can’t have.

The people who are the most vocal against real estate are the ones who have the most desire for real estate.

They are the activists who push government to enact laws that tax foreign buyers, tax absentee property owners, and build more housing because their rent is too damn high.

They are the bloggers who cherry pick a bad home sale to prove prices are weakening in an obviously booming city.

They are your friends and acquaintances who call you a trust fund baby, don’t believe you scrimped and saved all those years, or try to make you feel bad about your purchase.

To buy real estate responsibly, you need to go through these steps:

- Save enough for a 20% down-payment to avoid PMI.

- Have a financial institution deem you creditworthy enough to qualify for a mortgage.

- Make an attractive enough offer to be accepted by the seller.

- Have the guts to agree to the terms and take on the property.

At each stage, there is risk of rejection or failure.

It takes a lot of discipline and sacrifice to save $300,000 for a down payment on a median priced home in New York City. Therefore, most people don’t and get pissed at those who do. The human condition assigns luck to the achievements of others and skill to our own.

Due to more stringent lending standards since the financial crisis, the average credit score for those qualifying for a mortgage is over 720 (excellent). Banks also won’t lend to folks with a debt-to-income ratio of over 43%. If you get rejected for a mortgage, which has happened to me because I didn’t have two years worth of freelance income at the time, you will naturally hate the lender and housing in general.

In competitive housing market, it’s common to get rejected multiple times before finally giving an offer good enough to be accepted. Each rejection beats you down because you always dream about what your life would be like in the property you are pursuing. Get rejected enough and you’ll either put out some crazy high offer to your detriment or get really bitter at the entire process.

Once your offer is accepted, you need to muster up the courage to transfer a good chunk of savings into escrow and in most cases assume a mortgage. Plenty of people get cold feet and back out from their offer. It takes guts to take such concentrated risk. If you backed out only to see the property resell years later for lots more than you could have bought it for, of course you’re going to be pissed off.

Now let’s look at how difficult it is to acquire stock.

The barrier to entry to buying stock is pretty much ZERO. Robo-advisors like Wealthfront can build you a stock portfolio for free starting with just $500. You can open up a Fidelity brokerage account with $100 and buy roughly 70 ETFs commission free. There’s even a new fintech company called Robinhood that allows you to trade everything commission free.

When anybody and everybody can buy stock, stock simply becomes less desirable. When there is only one panoramic ocean view property in on a 10,000 square foot lot with a hot tub time machine owned by someone who will never sell, of course the property will be more desirable than any stock on the planet.

Why do you think there’s not nearly the same level of rage against owning stocks?

Think about this: It’s somehow OK to rent all your life and be short the housing market. Yet if anybody decided to short the S&P 500 index their entire life, they’d be considered a buffoon.

Other Reasons Why Real Estate Is Attractive

Now of course stocks have shown to be solid long-term investments over the long run, which is why I’ve got almost 1/3rd of my net worth in the asset class. But this is an article addressing the housing haters who believe real estate is a terrible investment, so let’s continue!

1) You are the CEO, not a minority investor. Every physical real estate investment you make puts you in charge. As CEO, you are able to make improvements, cut costs (refinance your mortgage), raise rents, find better tenants, and market accordingly. Of course you are still at the mercy of the economic cycle, but overall you have much more leeway in making wealth optimizing decisions. When you invest in a public or private company, you are a minority investor who is putting his or her faith in management. Sometimes managers commit fraud or blow their companies to smithereens while making mega millions for themselves.

2) Leverage other people’s money cheaply. Thanks to mortgage interest rates coming down for 30+ years, qualified real estate investors can borrow money at 30+ year lows. Given the cost of capital is lower, the returns tend to be higher. Cheap interest rates also attract more borrowers, bringing more liquidity to the real estate market, which in turn puts upward pressure on prices. Even if real estate only tracks inflation over the long run, a 3% increase on a property where you put 20% down is a 15% cash-on-cash return. At this rate, in five years you will have more than doubled your equity. Just don’t get caught being overly levered in a down market.

3) More tax advantages. Not only can you deduct the interest on up to $750,000 in mortgage indebtedness on your primary home in 2018 and beyond, you can also sell your primary home for tax free profits up to $250,000 for singles and $500,000 for married couples if you live in the home for at least two of the last five years. Thanks to depreciation, a non-cash expense, you can shield your rental income as well. All expenses associated with managing your rental properties are also deductible against your rental income. If you are in the 32% marginal federal income tax bracket or higher, all the more reason to own your primary residence.

2018 Federal Income Tax Rates

4) Tangible asset. Real estate is something you can see, feel, and utilize. Life is about living, and real estate can provide a higher quality of life compared to a rental that is not properly maintained. I always believe in buying real estate for living first, cash flow second, and principal appreciation third. With stocks, there is no utility unless you spend the dividends or sell positions to purchase something. As a majority investor, the feeling of owning my primary residence is 1000X greater than the feeling of owning this Macbook I’m typing this post on, despite owning $150,000 in Apple stock.

5) Easier to analyze and make better investment decisions. It is much more difficult to analyze a company’s income statement, cash flow statement, and balance sheet than it is to analyze a property’s financial statements. This is why it’s often better to just buy an S&P 500 index fund for your stock allocation and call it a day. If you buy an individual stock, it may do incredibly well, or you might lose your shirt because you misjudged competitive pressures. For example, anybody who bought Blue Apron stock at the IPO is now down 75% because they misjudged Amazon coming into the market and crushing them. Hopefully you owned Amazon instead. Anybody who bought Lehman Brothers or Enron lost everything. With real estate, it’s easier to estimate rental income, occupancy levels, new supply, job growth, and population growth.

6) Less visible volatility. Your house value could be tanking and you would never know it since there isn’t a daily ticker symbol. During the 2008-2009 downturn, I still got to enjoy my vacation property in Lake Tahoe 20 days a year even though its value was plunging. Meanwhile, looking at the TV or computer screen just made me mad at how much I was losing in my stock portfolio. When your investment is less volatile, it’s much easier to stay the course and not sell at the bottom.

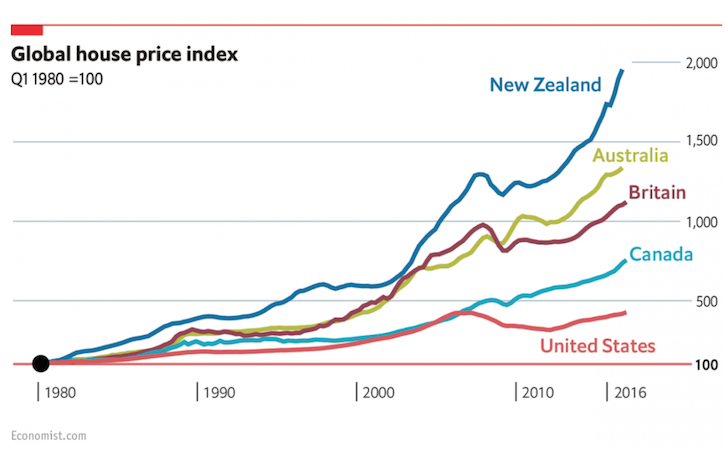

Go New Zealand go! Only 4.5X more expensive than the US

7) A greater source of pride. After a while, making money for money’s sake is a pretty empty feeling. Money needs to be used for something, such as buying real estate to raise a family. Every time I drive by my rental property I feel proud to have made the purchase in 2003. It reminds me of the time when I was 26 years old and still trying to make a name for myself at the job. I have zero sense of pride with my stock portfolio, partly because nobody sees it and nobody uses it.

8) More insulated. Real estate is local. If you’ve made a good decision to buy in an economically strong region, you will be more insulated from the national economy or the global economy. Look at prices in superstar cities such as NYC, Hong Kong, Singapore, London, Paris, and San Francisco. They fall the least, recover the soonest and gain the most. Of course if tech ever collapses, my real estate holdings will be crunched. Therefore, I sold one SF property and reinvested $500,000 of the proceeds in real estate crowdfunding projects everywhere else but San Francisco for diversification purposes.

9) The government is on your side. There are two organizations not worth fighting against: the Federal Reserve and the Central Government. Not only do you get generous mortgage interest tax deductions and tax free profits, the government sometimes bails out overextended homeowners during bad times. I got a free loan modification on my vacation property mortgage from Bank of America, even though I didn’t need it. The government forced BoA to cut my 30-year fixed mortgage from 5.875% down to 4.25%. Programs such as HARP 1.0 and HARP 2.0 allowed folks without hefty down-payments to get in on the action. There are plenty of non-recourse states such as California and Nevada which don’t go after your other assets if you decide to stop paying your mortgage and squat for months.

10) You’ll save your children from angst and despair. When you die, you can pass on your real estate holdings to your children using a stepped up cost basis to let them create their own memories, tax free. With the estate tax limit threshold now $11 million per person, you’ve got twice the room to pass on assets tax free than during the last administration. All the people who are anti-housing could have been saved if their parents decided to invest in real estate 30 years ago. Life is so much easier once housing is cheap or free. If you’re willing to provide an education for your children, perhaps you should also be willing to provide housing just in case they need it.

Real Estate FOMO Is The Illest

In a bull market, the average person’s day job income will likely never catch up with their local real estate market. For example, when the San Francisco median home price jumped from $1,000,000 to $1,100,000, the median income of $80,000 would have to jump 125% just to stay even.

The good thing is that real estate goes in cycles. You are finally seeing markets like Toronto, New York City, London, and San Francisco soften due to new supply, rising mortgage rates, residents moving away, and property prices that have far outstripped wage increases. Healthy downturns will usually last 2-3 years before stabilizing and then resume their upward trajectory.

Hopefully during soft times, folks who want to buy homes will have already aggressively saved and figured out ways to boost their income. Otherwise, it’ll be the same cycle of angst, anger, and despair over and over again.